{kind=link}

On-boarding new employees

With Australia now opening back up after the COVID restrictions, unemployment is tipped to fall to the lowest rate in just over 50 years – down to under 4%. If over the coming period you hire new staff, there are certain steps you should follow to cover off on your tax, workplace, and superannuation obligations.

- Confirm if the worker is legally permitted to work in Australia

Australian citizens, permanent residents and New Zealand citizens are legally permitted to work in Australia. If the worker does not fall into these categories, you must before employing them, confirm they have a visa granting them permission to work here. For more information, visit the Department of Home Affairs website https://immi.homeaffairs.gov.au/visas. - Employee or Contractor?

Establish the nature of the engagement – is the worker an employee or contractor? This matters from a tax perspective because employers will have PAYG withholding obligations to employees. By contrast, no PAYG withholding obligations are owed to contractors unless there is a PAYG voluntary withholding agreement in place. You and a contract worker (payee) can enter into a voluntary agreement to withhold an amount of tax from each payment you make to them. This is a good way to help independent contractors meet their tax obligations.

A voluntary agreement can cover a specific task or apply to successive arrangements between you and the worker. Either you or the contractor can end a voluntary agreement at any time by notifying the other in writing.

The employee/contractor distinction also matters for superannuation purposes. Employees are generally entitled to superannuation.

From 1 July 2022, this also includes employees who earn less than $450 per month. On the other hand, contractors are not entitled to superannuation unless they work under a contract that is wholly or principally for their labour.

While in many cases, the status of a worker may be clear cut, if as an employer you are in any doubt about the character of the relationship, then you are encouraged by the ATO to use their Employee Contractor Decision Tool. The tool asks the user a series of questions, and then reaches as a result depending on the answers provided. Print out the result and keep it on file.

If you need further guidance or disagree with the result, speak to your accountant. - Paperwork

Before commencing employment, employees should complete the following forms:

– TFN declaration – this is so employers can work out how much tax to withhold from employees.

– Standard super choice form – to offer eligible employees their choice of superannuation fund. Employers must fill in the details of their nominated super fund, also known as a default fund, before providing the form to an employee.

Note that employees can now access and complete pre-filled commencement forms through ATO online services via myGov. - Request stapled super fund

If you now take on a new employee and they don’t choose a super fund, employers will have an extra step to take to comply with the choice of fund rules. That is, employers may need to request an employee’s ‘stapled super fund’ details from the ATO. A stapled super fund is an existing super account linked, or ‘stapled’, to an individual employee so it follows them as they change jobs. This aims to reduce account fees. Employers can request stapled super fund details from the ATO using ATO online services. - Confirm pay rates

An employee’s minimum wages, including penalty rates, overtime rates, and allowances will in most cases be set out in the relevant workplace Award. Additionally, some employees have special minimum wages rates in their Award, for instance juniors, apprentices, and trainees. Contact Fair Work Australia on 13 13 94 if you are in any doubt about the applicable rates.

On the Fair Work front, employers are also generally required to provide new employees with a Fair Work Information Statement. - State and Territory Obligations

Other issues may be in play when you take on a new employee, such a workers’ compensation coverage.

Employee or contractor? If as an employer you are in any doubt about the character of the relationship, then you are encouraged by the ATO to use their Employee Contractor Decision Tool.

Paying employees super through a super clearing house

If you’re a small business owner, you’ll know that you’re required to pay your employees (and certain contractors) superannuation guarantee (SG) in addition to their salary or wages. But how do you pay your SG contributions in a simple and effective way? The answer is through a superannuation clearing house (SCH).

WHAT IS A SCH?

A SCH is an online portal that allows you to make all your super contributions for all your employees in one single payment.

The clearing house will then distribute the money to each employee’s super fund on your behalf and according to your instructions. This means using a SCH can save you time and also minimise the risk of payment errors.

WHY DO CONTRIBUTIONS HAVE TO BE MADE ELECTRONICALLY?

Back in 2012, legislation was passed to make electronic payment of super compulsory. This was done to reduce the number of missing and lost super payments and make managing and reporting on payments simpler for businesses. As a result, employers must send contribution payments and data electronically in a standard format called ‘SuperStream’. SuperStream transmits money and information consistently across the super system between employers, funds, service providers and the ATO. The data is linked to the payment by a unique payment reference number.

WHERE DO I FIND A SCH?

There are a few options available when paying super to employees’ super funds which meet the SuperStream requirements. These include:

■ Using a payroll system which is in line with SuperStream requirements, such as MYOB and Xero.

■ Using your employer-nominated super fund’s clearing house – most super funds provide access to a SCH service and will help you set up your account.

■ Using the ATO’s ‘Small Business Super Clearing House’ (SBSCH) – this free service is available to small businesses with 19 or fewer employees, or a turnover of less than $10 million a year.

■ Using a commercial SCH of your choice – there are a number of private/commercial SCH service providers but they do generally come at a cost.

WHAT TO CONSIDER WHEN CHOOSING A SCH

Below are points to consider before choosing a SCH:

■ Is the SCH SuperStream compliant? It may be worthwhile looking for another SCH if your preferred SCH does not meet the Government’s SuperStream and Single Touch Payroll requirements.

■ Is there a cost? If you’re using a payroll system that offers a similar service to a SCH, there may be fees involved to use this software. If fees apply, check if the charge is per employee or per transaction as this will allow you to estimate your annual cost. Other SCH services can be a low or no-cost option, so it’s best to research the costs involved (if any) before you choose a service.

■ How long does it take to process payments? The time it takes for your payment to be processed by the SCH and deposited into employee super fund/s must be considered. For example, if you use the ATO SBSCH and provide the ATO with all of the required information, payments may take up to seven business days to be transferred through the clearing house before they reach employee super fund accounts. Thus, choosing a SCH that processes payments quickly and efficiently may minimise the number of enquiries from your employees.

■ Does the SCH automatically validate employee information? It is worthwhile asking the SCH if they use the Australia Post database to automatically validate employee addresses. This will minimise the chance of errors and speed up processing times.

In-specie super contributions

Most contributions to a SMSF are made in cash, but did you know you can also contribute certain assets to your fund too? These types of contributions are called “in-specie” contributions and may be a good alternative to consider if you don’t have available cash on hand and want to make a contribution to super.

What assets can be transferred in-specie to super?

While most superannuation funds can accept in-specie contributions, they occur more commonly with SMSFs than with industry or retail superannuation funds.

But only certain assets listed in the super laws can be transferred to an SMSF from a member of the fund.

Most in-specie contributions are made using:

■ Listed securities on an approved stock exchange (ie, ASX listed shares)

■ An investment in a widely-held trust (ie, a retail managed fund), and

■ Business real property (ie, where land and buildings are used wholly and exclusively in a business).

Treatment of in-specie contributions within the SMSF

Regardless of whether the contribution is made via cash or in-specie, in many respects they are treated in much the same way – for example:

■ The standard work test for super still applies – eg, the member making the contribution must meet certain age and employment requirements in order to make the contribution

■ The in-specie contribution will be counted toward the relevant contribution cap(s) in the same way, and

■ In-specie contributions may result in a member being eligible to claim a personal tax deduction for some/ all of the contribution, based on the usual eligibility criteria.

For example, if business real property is valued at $530,000 and it is transferred to an SMSF with its entire value considered a contribution, it could result in an excess non-concessional contribution of $200,000.

To avoid this outcome, you could:

■ Treat $330,000 of the in-specie transfer as a non-concessional contribution under the three-year bring- forward rule, and

■ Treat the remainder as an asset sale.

Here, the SMSF will pay you the market value of the asset being transferred by transferring $200,000 of cash or other assets owned by the fund to effect the sale on that portion of the property – keeping the member under the non-concessional cap.

When you make an in-specie transfer to your SMSF, it can be treated as either a contribution (ie, non-concessional or concessional contribution) or as an asset purchase by the SMSF.

Having an in-specie contribution treated as an asset purchase can be beneficial where the value of the asset is greater than the contribution caps available to the contributing member.

Benefits of making in-specie transfers

Making a contribution of assets rather than cash can benefit SMSF members as it allows them to increase the value of their retirement savings by transferring the aforementioned assets they already own into superannuation without the need to sell the asset first.

Where that asset is a property, such as business real property, it can then potentially be leased back to a related party of the fund to use in a business.

Points to consider when making in-specie transfers

As mentioned above, SMSFs can only accept certain types of assets, such as listed shares or business real property, as an in-specie contribution from a member. This rule therefore limits the types of assets that can be transferred to your fund. For example, a residential property you own personally cannot be transferred to your SMSF.

Further, because there is a change in ownership of the asset transferred from the member to the SMSF, the transfer is deemed to be a disposal for the member and any gain realised may be subject to capital gains tax.

The SMSF may also incur stamp duty and transaction costs when the asset is transferred to the fund.

What about in-specie transfers out of the fund?

Assets can also be transferred out of the fund as in-specie payments, although only lump sum payments can be made in-specie. If you are in pension phase, pension payments have to be made in cash. However, the rules on acquisitions from members do not apply to these transactions as the SMSF is disposing of the asset, not acquiring it.

Check your trust deed

Before attempting to make an in-specie contribution to your fund, its best to check your SMSF trust deed to confirm if you are allowed to make in-specie contributions and whether there are any rules or restrictions around what assets members can make as an in-specie contribution.

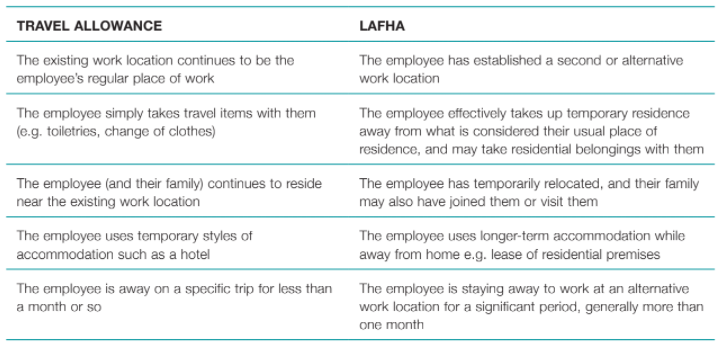

Employee allowances

Do your employees travel for work? The ATO has issued new guidance to help employers determine whether to pay employees a travel allowance or a living-away-from-home allowance (LAFHA).

There are some key differences between the treatment of the two types of payments:

■ A travel allowance will generally need to be included in your employee’s assessable income and may need to have tax withheld from it. It covers accommodation, food, drink or incidental expenses an employee incurs when they stay away from their home overnight or for a short period to carry out their duties. It’s generally deductible to the employer.

■ A LAFHA payment you provide to your employees may be considered a LAFHA fringe benefit. Where this is the case, it will need to be reported in your annual fringe benefits tax (FBT) return. LAFHAs are paid to compensate an employee for additional living expenses they incur if they are required to live away from home for an extended period for work purposes. In certain circumstances, such payments may be exempt from FBT for the employer and not taxable to the employee!

LAFHAs are paid where an employee has moved and taken up temporary residence away from his or her usual place of residence so as to be able to carry out their job at the new but temporary workplace. The employee has a clear intention/expectation of returning home on the cessation of work at the temporary location (in this sense, the employee is absent for a limited/finite period of time).

On the other hand, a travel allowance is paid for specific trips because the employee is travelling in the course of performing their employment duties but has not temporarily relocated as a LAFHA recipient would. The existing work location continues to be the employee’s regular place of work. In travelling away from home, the employee simply takes travel items (such as toiletries and a few changes of clothes). Employees receiving a travel allowance will also typically use temporary styles of accommodation such as hotels.

A travel allowance provided by an employer is not taxed under the FBT regime but may be taxed under the PAYG withholding regime as a supplement to salary and wages. The ATO publishes guidelines each year on what it considers to be reasonable amounts for a travelling employee, and take the following factors into consideration:

■ destination of travel (broken down into metropolitan cities, country centres within Australia and international countries)

■ accommodation

■ meals

■ other incidentals

■ employee annual salary (in ranges)

■ specific rates for truck drivers.

Countries other than Australia are split into “cost groups”, with each determining the reasonable amount of the daily allowance. These are determined based on the cost of living in that country and then numbered between cost groups one to six. Cost group one has the lowest daily allowance and cost group six has the highest.

The reasonable amounts are intended to apply to each full day of travel covered by the travel allowance, with no apportionment required for the first and last day of travel.

Where the employer has paid the employee less than the ATO-determined reasonable amount, then the employer is not obligated to withhold from the allowance nor does the employer have to include the allowance on the employee’s PAYG income statement.

Key differences between the two types of payments are captured in the table on the following page.

Ultimately, allowances for travel are a handy employee retention tool – helping them cover the costs of work-related expenses they may incur while travelling on or relocating for business. Speak with your advisor if you are uncertain about their taxation treatment.

Key differences between travel and living-away-from-home allowances

Cashflow forecasts

Now more than ever businesses should consider preparing cashflow forecasts.

According to the Australian Bureau of Statistics, half of all small to medium businesses fail in the first three years of operation. The Australian Securities and Investment Commission states that poor cash flow is cited as a factor in 40% of business failures. Indeed, as Australia emerges from an economic recession, cashflow will be a key issue for all businesses – not just start-ups.

All businesses must ensure they have sufficient cash, at a particular time, to pay their bills. Cash is needed constantly in order to discharge a wide range of payment obligations which arise from many sources, including:

■ the ATO

■ suppliers

■ banks

■ employees, and

■ insurers.

A cashflow forecast is a crucial cash management tool for operating your business effectively. Specifically, a cashflow forecast tracks the sources and amounts of cash coming into and out of your business over a given period. It enables you to foresee peaks and troughs of cash amounts held by your business, and therefore whether you have sufficient cash to fund your debts at a particular time.

Moreover, it alerts you to when you may need to take action – by discounting stock or getting an overdraft, for example – to make sure your business has sufficient cash to meets its needs. Cashflow forecasts also allow you to see when you have large cash surpluses, which may indicate that you have borrowed too much, or you have money that ought to be invested.

In practical terms, a cashflow forecast can also:

■ensure your business is funded adequately

■ improve your credit rating and ability to secure finance

■ assist in the planning and re-allocation of resources and

■ see the impact of financial decisions before you make them

At this point, a distinction should be drawn between profit budgets and cashflow forecasts. While budgets are designed to predict how viable a business will be over a given period, unlike cashflow forecasts, they include non-cash items, such as depreciation, and exclude some cash payments, like the principal portion of loan payments. By contrast, as stated above, a cashflow forecast focuses on the actual cash in, and cash out of a business over a given period. In short, budgets will give you the profit position; cashflow forecasts will give you the cash position. it is important to understand the difference.

A cashflow forecast is usually prepared for either the coming quarter or the coming year. When you are preparing forecasts, it is important to use realistic assumptions. This will usually involve looking at last year’s results and combining them with economic growth, and other known factors affecting your business.

Usually a forecast will list:

■ Trading and capital receipts

■ Trading and Capital payments

■ excess receipts over payments (or otherwise)

■ opening and closing bank balance

If you are uncertain of how to prepare a cashflow forecast, consult with us because we are experts!

RAT and PCR Tests

Favourable tax treatment for employers

Finally, some good COVID-19 news (at least on the tax front) for employers!

Ever since the arrival in Australia of the Omicron variant in late 2021, the recommended test for detecting COVID has been the rapid antigen test (RAT). Indeed, for some employees, returning a negative RAT has been an ongoing condition of returning to work. As a result, there has been a massive buy up of these tests by both employers, employees and by others – often at significantly marked up rates. On the tax front, relief is now at hand!

ANNOUNCEMENT

In a press release dated 8 February 2022, the Assistant Treasurer announced that COVID19 tests (including Polymerase Chain Reaction (PCR) and Rapid Antigen Tests (RATs)) are now tax deductible, and exempt from FBT for employers, where they are purchased for work related purposes. This will apply both when an individual is required to attend the workplace or has the option to work remotely.

CURRENT LAW

The new law is aimed at clearing up the confusion which exists, created in part by the government claiming for some time that the tests were deductible, despite it being doubtful under the current income tax rules at least as they relate to individuals.

The new law will also clarify the existing doubt under the current FBT law. Currently, to not pay FBT employers would need to rely on one of the following:

Draft legislation has not been released at the time of writing this article. It will be interesting to see if pressure is put on the government to extend the exemption to masks and other personal protective equipment which, somewhat inconceivably, remain potentially subject to FBT.

FBT can be a complex area. Talk with your advisor if you are uncertain about what this means for your business.

FURTHER DETAILS

Under the new law if an individual had to purchase RATs to be able to work, they will be able to claim a tax deduction for the cost they incurred from 1 July 2021 (they will also need evidence of the expense). If the RAT cost $30, an individual on a marginal tax rate of 37% would enjoy a tax deduction of $7.40.

By contrast, if a test was not required for work, for example an individual just had symptoms but was not required by their employer to get a negative test before returning to work, then the cost will presumably not be deductible.

Employees and employers should retain evidence of their COVID expenses in order to take advantage of these new rules.

{kind=link}

{kind=link}

{kind=link}